Thanks to the introduced tax on wells and wells, the legislation of the Russian Federation controls the use of water resources, as well as on which territory and by whom they are used. In addition, at the expense of it, those who engage in illegal extraction of water are found. That is, taxation allows you to control the environmental situation in the state. There are also more frequent cases when a special license is required for the exploitation of water resources (for example, for tubular-type wells). It can be obtained from the executive authorities by preparing the necessary package of documents and filling out an application.

For each water source you must have those. passport, which contains all of its characteristics provided after construction to the Department of Supervision of the Russian Federation. And he, in turn, already determines the need for payment, and the amount of water that can be consumed (some types of wells are subject to a limit on the amount of water used).

For each water source you must have those. passport, which contains all of its characteristics provided after construction to the Department of Supervision of the Russian Federation. And he, in turn, already determines the need for payment, and the amount of water that can be consumed (some types of wells are subject to a limit on the amount of water used).

Pay for the use of water that is extracted from a well or well in the following cases:

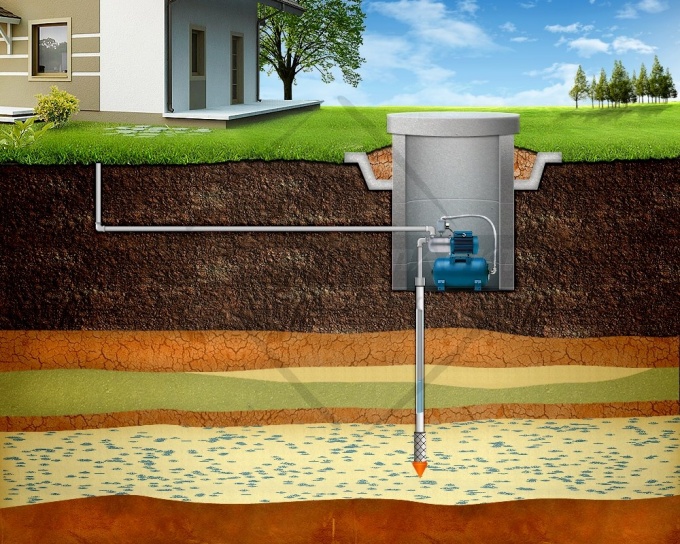

- If the source has a depth of 40-250 meters;

- Water contains a high concentration of natural salts and minerals;

- The composition of water does not have various metal impurities;

- The mine is drilled into the lower layer of the water core.

Water use tax is not subject to the following conditions:

- The depth of the source does not exceed twenty meters (in some cases forty meters);

- A well or a well is installed on a summer cottage or personal territory;

- The owner of the source does not use it for entrepreneurial activity;

- A well or well does not affect the water of natural resources;

- The amount of water used does not exceed the established norms calculated for residents of the house and watering the territory;

- Wells located on limestone do not affect central water supply.

Subject to the above conditions, the use of water will be unlimited, or special control bodies will conduct an appropriate check (which they can carry out at any time) and in case of violations, the owner may be issued a warning or a fine. In case of repeated violations, the well will be ordered to shut off.

Regulatory laws

Subparagraph 13 of paragraph 2 of Article 333.9 of the Tax Code of the Russian Federation indicates the absence of taxation for the use of water, provided that it is used only for irrigation of summer cottages and other personal needs of the owners.

Subparagraph 13 of paragraph 2 of Article 333.9 of the Tax Code of the Russian Federation indicates the absence of taxation for the use of water, provided that it is used only for irrigation of summer cottages and other personal needs of the owners.

Law No. 2395-1 “On Subsurface Resources” indicates the possibility of using water from wells and wells to irrigate one’s own land and watering livestock and ordinary animals.

Law No. 3314-1 “On the Procedure for Enactment of the Regulation on the Procedure for Licensing the Use of Subsurface Resources” contains the procedure for licensing and operating wells. It consists of all types of sources for which tax is required or vice versa.

Clause 3 of Article 7 of the Administrative Code of the Russian Federation contains the amount of penalties that are imposed for the operation of an unregistered source.

In case of violations, rather large fines are issued:

- For directors of companies - from 30 to 50 thousand rubles.

- For jur. persons - from 88 to 100 thousand rubles.

- For physical. persons - 3000 to 5000 rubles.

Terms of payment of tax and its size

An artesian well is the most important and key source, as it has a strategic supply of clean water, and therefore is considered to be natural wealth, as well as minerals, due to this, the cost of its use is quite high.

An artesian well is the most important and key source, as it has a strategic supply of clean water, and therefore is considered to be natural wealth, as well as minerals, due to this, the cost of its use is quite high.

But the price in this case is not a constant, but rather quite different, since it depends on many criteria (even on the location of the source).

- For the use of water for personal purposes, individuals pay 81 rubles. beyond 1000 m3;

- Water supply facilities, individual entrepreneurs and businessmen pay at completely different rates, the size of which can be from 300 to 754 rubles per 1000 m3 (all prices can be clarified by the Federal Tax Service or on its official website).

In any case, there is a restriction of use for everyone, above which the tax rate increases 1.15 times. All data can also be viewed on the FNOS website or by visiting the office in person.

Everyone is required to pay taxes no later than the 20th day of the following month after the last quarter. That is, on January 20, April, July and October, all payments must already be made.

After each payment made, it is necessary to provide a confirmation report to the Federal Tax Service Inspectorate at the place of registration of the water intake.

In case of delay in payment, as in any other cases, a fine will be charged in the form of a penalty.

Submission of a declaration

According to the legislation of the Russian Federation, there is a special procedure for the declaration of payment of tax for the use of water.

Before starting the whole process, you need to prepare a standard package of documents that will be required at the Federal Tax Service Inspectorate. This list consists of:

- Journal of water level control;

- Tax return (prepared independently);

- A license that allows you to operate or drill a source (to obtain it, you must also prepare: a cadastral document, a certificate of the water analysis; data on the restriction for pumping, a water level control log and copies of all packages of documents);

- Passport of a well or well;

- Conclusion on the sanitary zones.

Now we are preparing a tax return consisting of a title page and several paragraphs that contain the following information:

- Tax value;

- All necessary calculations (tax base, water tax cost, etc.).

Such a declaration is valid only in one tax period. With its proper preparation, the tax is recalculated, but the checks carried out by specialized services will not be taken into account.

The declaration can only be submitted on paper (not accepted electronically). All data must be completed by hand, but you can print the document on the printer. After it is signed by authorized persons of the Federal Tax Service and certified with a seal.